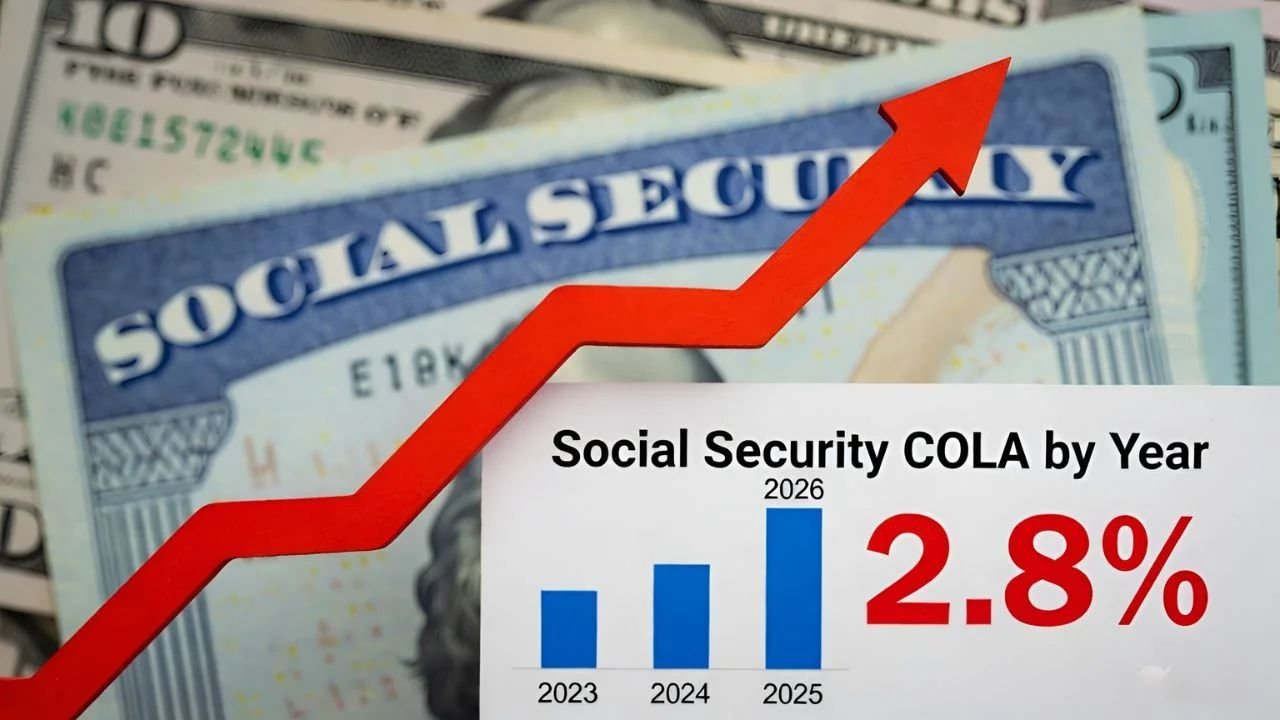

Millions of retirees across the United States are preparing for the next Social Security cost-of-living adjustment, commonly known as COLA. Early projections suggest benefits could rise by around 2.7% to 2.8%, a modest improvement over the previous year’s adjustment.

At first glance, any increase is welcome news for older Americans who rely heavily on Social Security to cover everyday expenses. However, economists and retirement analysts warn that the actual financial relief many seniors feel may be smaller than expected.

The reason is simple: rising healthcare costs, Medicare premiums, and everyday living expenses are increasing at a similar or faster pace.

Understanding the Latest COLA Projection

Cost-of-living adjustments are designed to help Social Security payments keep up with inflation. The increase is calculated using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a federal measure tracking price changes in key consumer goods.

With a projected increase of around 2.8%, retirees receiving the average monthly benefit could see a small boost in their payments.

Estimated Monthly Benefit Changes

| Average Monthly Benefit | Approximate COLA Increase | Estimated Monthly Gain |

|---|---|---|

| $1,700 | 2.8% | $48 – $50 |

| $2,008 | 2.8% | $54 – $56 |

| $2,500 | 2.8% | $70 |

While these increases provide additional income, the final amount retirees receive after deductions could be lower.

Medicare Premiums Could Reduce the Real Gain

One of the biggest factors affecting retirees’ take-home Social Security payments is Medicare.

Rising Healthcare Costs

Medicare Part B premiums are expected to increase again, with estimates suggesting the monthly premium could reach roughly $206. Because these premiums are automatically deducted from Social Security benefits, they directly reduce the net increase retirees receive.

In some cases, analysts estimate that up to 40% of the COLA boost could be absorbed by higher Medicare costs.

For example, a retiree expecting a $54 monthly increase might ultimately see only about $32 to $33 after healthcare deductions.

Inflation Continues to Pressure Retiree Budgets

Another reason the adjustment may feel smaller is the way inflation impacts seniors differently from the general population.

The CPI-W index used to calculate COLA focuses on spending patterns of working households. However, retirees often spend a larger portion of their income on healthcare, prescription drugs, housing, and utilities.

These categories have seen particularly strong price increases in recent years.

Even during years with historically large COLA increases—such as the adjustments seen earlier in the decade—many retirees reported that their purchasing power barely improved.

Financial Pressure on Fixed-Income Households

Many older Americans rely on Social Security as their primary or even sole source of income. Without additional retirement savings or pension income, even small cost increases can strain monthly budgets.

This combination of moderate COLA adjustments and rising living expenses is sometimes described by economists as a “double squeeze.”

Seniors face higher everyday costs while their benefits grow more slowly than those expenses.

Additional policy changes may also affect retirement finances, including adjustments to retirement age rules, earnings limits for early retirees, and taxable wage thresholds.

Policy Ideas Being Discussed

Policymakers and retirement advocates have proposed several measures aimed at protecting low-income retirees from financial strain.

Potential Support Measures

| Proposal | Goal |

|---|---|

| Expanded Medicare subsidies | Reduce healthcare cost pressure |

| Caps on out-of-pocket medical spending | Protect retirees with chronic health needs |

| Improved low-income assistance programs | Ensure benefits reach vulnerable households |

| Alternative inflation index for seniors | Reflect real retiree spending patterns |

If implemented, these policies could help ensure that COLA adjustments provide more meaningful financial relief.

What Retirees May Consider Going Forward

Financial advisors often encourage retirees to regularly review their budgets and plan for changing expenses.

Strategies such as delaying Social Security benefits, managing healthcare costs carefully, or exploring supplemental retirement income sources can help strengthen long-term financial stability.

Staying informed about benefit changes and healthcare costs is also essential for navigating retirement with confidence.

The Bottom Line

The projected Social Security COLA increase will provide a modest boost to monthly benefits. For many retirees, however, the improvement may feel limited once healthcare costs and everyday expenses are factored in.

While the adjustment reflects efforts to keep benefits aligned with inflation, the broader challenge remains ensuring that retirees maintain their purchasing power in an environment of rising costs.

As policymakers continue evaluating solutions, the balance between benefit growth and real-world living expenses will remain a key issue for America’s aging population.